You know that real estate bubble I keep saying is inflating? It just got a pump of air. I agree with Jim Morrison at Banker and Tradesman that easing credit restrictions is the wrong thing to do. It didn’t go well in 2006, and it won’t end well this time.

What’s happened?

What’s happened?

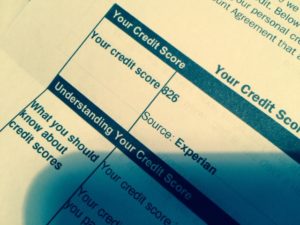

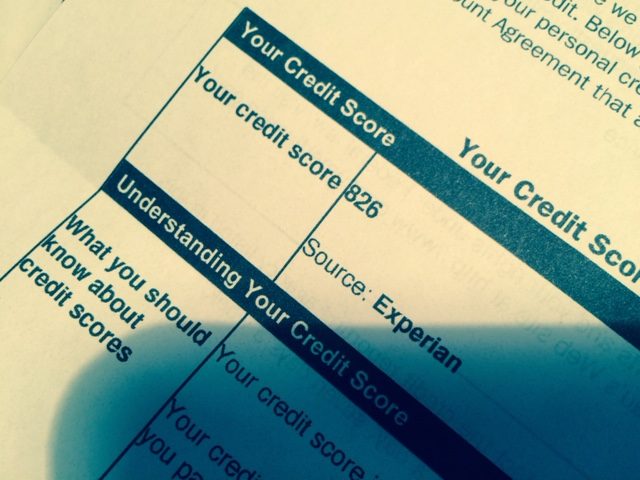

Credit reporting has changed. CNBC explains that the three big credit scoring companies will no longer look at civil judgments and tax liens as part of a credit score. The rationale is that consumers complain that there are inaccuracies in their credit reports in these matters.

What’s a civil judgment? It’s a debt owed because of a non-criminal court matter. Examples include a judgement where a judge agreed that you owed for an unpaid utility bill. It could be a small claims court matter that has not yet been paid (or not cleared in the record as fully paid). Some of these matters can linger for years, as long payment schedules are paid off. People who have civil judgments against them can have long periods when they have a big ding on their credit score. Not anymore.

What’s a tax lien? The IRS can get a tax lien if you owe back taxes. This allows them to collect back taxes from your business or property. It is does not necessarily force you to sell; it allows the Treasury rights as a creditor, and has attached your property or business.

Who benefits? People who had low credit scores that will no longer have bad credit scores. Example: People who have judgements or tax liens will see an increase in their credit scores.

- Higher scores will allow them to borrow.

- Higher scores allow them to borrow at a lower interest rate (since they will look more credit-worthy with this new, higher credit score.)

Who loses? People who have good credit scores before this loosening of standards.

- More people will be able to borrow. This increases the pool of consumers who borrow to purchase goods and houses. Therefore, consumer demand goes up, and prices go up.

- Lenders will have a riskier pool of borrowers, who they can no longer distinguish from people who did not have judgements or tax liens. This will give lenders justification to raise their interest rates for all

- Right now, the last thing the metro Boston real estate market needs is more demand! Our clients just lost.

Other economic factors:

Other economic factors:

Just two weeks ago, I wrote about housing affordability. RIS measured that median income was not enough for median housing in our region. If you missed that, here.

Jim Morrison, in an earlier Banker and Tradesman blog notes that the concentration of home ownership compared to rental is at 63.7 percent. Healthy level is 64-65 percent. Too low indicates a sluggish real estate economy and too high (as in 2005, when it was 69.1 percent) can be a harbinger of speculative buying and a foreclosure crisis ahead.

Takeaway: There is more evidence that we are approaching the top of the market. Buy carefully.

Leave A Comment